Novice Investor #21 - SaaS DCF Valuation, Generative AI and the Neoclassical Growth Theory

It is the start of 2023 and it feels like we are heading into an exciting year. Are we through the worst of the hard times or are we headed into a death spiral of layoffs and higher inflation? With most media outlets and economic experts saying a deep recession is inevitable, the contrarian in me is remaining cautiously optimistic. Irrespective of how the economy performs, backing solid, capital-efficient software businesses minus the crazy ARR valuation multiples seems like a good strategy.

Here are a few reasons why I am bullish for the years ahead:

Capital efficiency is back in vogue. During 2020 and 2021, growing your SaaS business in a capital-efficient manner was an afterthought. Today, most software companies have a board-approved budget chasing towards break even. More discipline on costs has created a larger pool of high-quality prospects and increased investor-founder fit.

With crisis, comes opportunity. For companies who didn’t over-stretch and are still hiring. There is plenty of great candidates available with worthless options at over-invested companies. Hiring top managers should be a lot easier.

Generative AI - More info below

We kicked off the year with another Kennet Event. Earlier this month Pete Daffern gave a great talk on the 10 Key Traits of a Great CEO at the Goodman Gallery in Mayfair. If you are interested in joining future events, do let me know.

Novice Investor SaaS DCF

Valuing a SaaS business has always felt like a bit of a dark art to me. In my earlier career through M&A advisory and reading CFA books, I received plenty of experience in logically valuing businesses with detailed models, WACC calculations and cashflows. Then, when entering the world of SaaS, everyone’s approach to valuing companies, rightly or wrongly, went back to kindergarten with simple Revenue or ARR multiples.

In my view, a business is an asset that generates future cash flow and should be valued as such. Unfortunately, the nature of high-growth SaaS companies makes this extremely difficult. For example, when valuing an energy infrastructure asset such as a wind farm, you know your capex requirements and costs with a high degree of accuracy, your annual utilisation is easy to predict, your price per unit of energy can sometimes be quasi-contracted for five years plus and you can be reasonably sure the annual revenue isn’t going to grow by more than 30%-50% over the life of an asset. This plus your own cost of capital is enough to get a pretty narrow and accurate valuation range all based on sensible cashflow assumptions. Compare this to a SaaS company. In five years, your revenue could be $50 million or $3 million and your cost forecast has equal volatility. This makes valuing a SaaS business on cashflows, using a traditional DCF model, nonsensical and hence why people revert to finger-in-the-air valuation methods of revenue multiples.

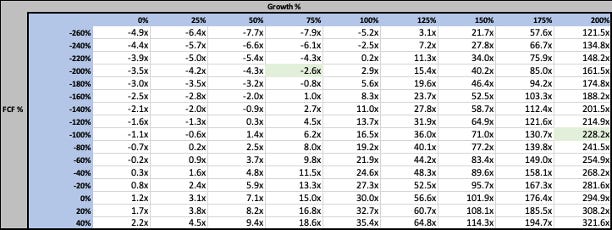

I created a basic DCF valuation model with the outputs above to illustrate this. The drivers are ARR growth and FCF margin. As you can see, very few of the valuation outputs make sense. Here are the issues:

High growth is too high - If I meet a business growing 200% with an FCF margin of negative 100%, there’s no way I am paying a 228.2x ARR multiple.

Overly penal on short-term high burn - Some Series-A stage businesses invest aggressively to expand the team and future growth. They could be growing 75% and easily clock a negative 200% FCF margin. Is a business like this really worth a negative 2.6x ARR multiple?

In general, very few of the output valuations make a whole pile of sense for SaaS businesses. So best off sticking that finger in the air and using revenue multiples right? Perhaps, but no harm in some excel fun to back up your kindergarten valuation techniques.

Introducing the Novice Investor SaaS DCF. It uses slightly more inputs, ARR Growth %, Free Cash Flow %, Net Revenue Retention % and Gross Margin to drive the valuation. The other two key differences are:

Normalised Inputs - This model uses the projected inputs in two years times. This puts an inherent bound on the inputs which normalise the valuation ranges. If you are a Series A company growing 300% off a small base due to a great year, there’s close to a zero % chance you will be growing 300% in two years. Plus if you have short-term high burn this won’t affect your valuation as much.

Hypothetical Termination of Growth Investing - The model assumes your current New Business sales team stays as is. They produce at the same monthly rate they did in your Year 2 projections. Additionally, your cost base remains flat. This assumption essentially asks, what would the cashflows be worth if we stopped investing further in growth to generate cash flow? This puts a bound on the crazy high valuations while still giving credit for strong growth.

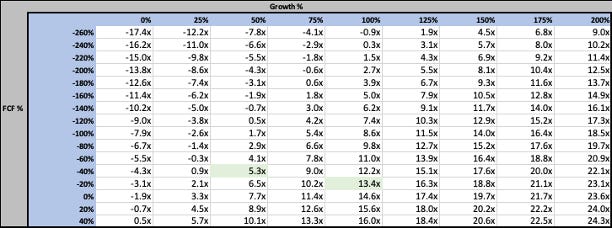

Let’s compare the results of the prior two examples:

200% ARR growth at negative 100% FCF %. This company will likely have an operating plan of reduced growth and better FCF % in two years, say 100% growth and a negative 20% margin. This generates a much more sensible 13.4x ARR multiple. Even if they maintained the 200% growth in two years, the ARR multiple would be high at 18.5x. However, if you can genuinely maintain a 200% growth rate for two years you should be worth at least 18.5x, but not 228.2x 😅

75% growth at a negative 100% FCF %. An operating plan an investor could reasonably back would be a 50% growth business with a negative 40% FCF in two years. This normalisation of inputs gives credit for the highly volatile nature of SaaS P&Ls and generated a pretty reasonable 5.3x ARR multiple, compared to negative 2.6x using the traditional method.

What about all the negative valuation outputs in this model? If you are running a business and plan to be growing at 25% in two years and generating an FCF % of less than negative 40%, you won’t be able to raise money so your valuation should reasonably be zero (from a cashflow perspective at least).

The final point worth noting when valuing businesses using this method is the difference in today’s metrics and the metrics in two years. You have to use conservative projections you believe will happen. Otherwise, you might want to discount the multiple.

This model is my own unreviewed excel pondering. I would love to get feedback on how you would improve or discredit the method. If you are up for an excel/valuation debate, please reach out.

Neoclassical Growth Theory and Generative AI

Taking a step back to my university days while learning about oversimplified macroeconomic theories, the Neoclassical Growth Theory always resonated with me.

The Neoclassical Growth theory aims to predict the long-term growth rate of any country. It uses three basic inputs to determine economic growth (Y) which are the availability of labour force (L), the availability of capital (K) and the state of technology (T).

Y = TF(K,L)

Interestingly, it bakes in diminishing returns of capital. For example, if a country has 100 people to work and very little capital (i.e. doing all work with hands) an increase in capital (to buy machinery) will have a big increase in economic output. However, if said country is already saturated with capital, a further increase in the availability of capital will do very little to increase economic growth. An increase in the labour force will have an increase in economic growth as there will be more people to use the capital to create output, although it will only increase linearly with labour force growth. The final and most interesting input into the theory is the state of technology (T). This has a boundless contributing factor to economic output. Irrespective of the state of the labour market or capital availability, technology is the key factor that can drive real long-term economic output.

By historical standards, most countries today, seem capital saturated (even with the recent interest rate increases). Contrastingly to the recessionary pundits, the labour force remains incredibly tight and slowing population growth doesn’t give me hope for the availability of labour force driving our economy long term. So that leaves us with one last hope for continued prosperity, Technology.

Looking back over the decades, we have had meaningful needle moves in terms of technology innovation which undoubtedly helped grow global economic output. Think the Internet, Moore's Law, the iPhone and the proliferation of Software. Although for the past five years, it seems all we have had in the innovation pipeline was over-hyped moonshots that struggled to produce value - Blockchain, Metaverse, Quantum Computing and previously, Artificial Intelligence.

Introducing Generative AI. The release and incredible traction generated by Chat GPT seem like a fulcrum point in AI finally generating significant value. Previously the technology was great at beating human Chess or Go champions but Alexa couldn’t even find my playlist on Spotify. Now AI can write content, provide expert advice, create beautiful art, edit videos, and much more.

Although numerous recession clouds are gathering, I see Generative AI as a glimpse of sunshine that will hopefully push economic growth over the next 5 - 10 years. What about people that are going to lose their job you ask? I’m sure plenty of us knowledge workers will be affected as generative AI is used more and more. Speaking for myself, if AI takes my job, I’m not going to sit around idly. I’ll find another opportunity, use the technology and capital available at the time and create economic value. If other knowledge workers feel the same, the Neoclassical Growth Theory suggests this could be a positive driver of long-term economic output.

Productivity Tech - Generative AI

The golden age of productivity tech is well and truly here. I mentioned the exciting things happening with the open-source GPT-3 model by Open AI a couple of times last year. Now with the release of chat GPT, the use cases and traction of the application have exploded. This will cause two things in my opinion, (1) massive customer demand, tech buyers around the globe will now ask themselves, could AI do this? Which will lead to plenty of customer enquires to AI businesses (2) a tsunami of generative AI startups will be and are being created as we speak. Think how alluring it is to whip up a generative AI MVP as a founder. Instant high-value applications that are extremely easy to build and sell. Fierce and undifferentiated competition is pending everywhere!

Irrespective of whether the generative AI space is a good place to invest (maybe I’ll speak about this in the next issue), the two points above will and have created a plethora of extremely cool, high-value productivity tools that I plan to test and use in my everyday.

Going back to my previous point of AI taking our jobs, I am not too worried about this. My sense is those who embrace, learn and creatively use AI to make themselves more efficient, will progress in their careers over the next decade. The Luddites out there will simply be at an ever-growing disadvantage which could result in termination. Don’t be a Luddite!

But how?

Test, learn and experiment with new tools. I’ll be sharing the tools I’m testing and using here. A foundational place to start is a free online course I completed last month called Learn Prompting. It gives a quick crash course on Prompt Engineering, which is a new word coined to describe the art of getting large language models like Chat GPT to do what you want.

Kennet Partners’ Investment Target

Kennet Partners is a Growth Equity investor with over 20 years of experience partnering with European and US SaaS companies. If you know any companies which fit our criteria, please reach out.

Investment size: $8m - $30m

Maturity: Over $3m in ARR

Growth: > 30%

Type: Bootstrapped and capital-efficient B2B SaaS businesses

Geography: Europe & US

Disclaimer: None of the content in the Newsletter should be taken as financial advice.