Novice Investor #22 - Scorecard SaaS Valuation Method, Has the Tech Crash Ended and Metaverse Revival??

Novice Investor #22 - Scorecard SaaS Valuation Method, Has the Tech Crash Ended and Metaverse Revival??

Happy July All,

I hope everyone is enjoying the Summer.

It has been a full 18 months since the Nasdaq hit its last peak and we entered the latest large-scale tech repricing event. The Dotcom crash took 30 months for the Nasdaq to hit a trough, while The Great Financial Crash took 17 months. Have we already reached the bottom or is there more to come?

I’m going to continue with my Neoclassical Growth Theory / AI will drive economic growth assumption from the last post in February and guess the bottom was already hit in January of this year (13-month crash). The Nasdaq has increased over 20% since February, mainly due to the big tech companies with AI plays (Microsoft, Google, Nvidia etc.).

While growth levels are still depressed for non-AI software, I still think now is a great time to invest if you can find a quality opportunity. Who is raising?

Special shout out to Mark Sheperd and his latest move with the London Tech Drinks. I attended a summer event last month, which as always, was a great place to network with other investors. Mark recently announced he’s going full-time on the company. If you want to attend any of his events, sign up here. Good luck to Mark!

Scorecard SaaS Valuation Method

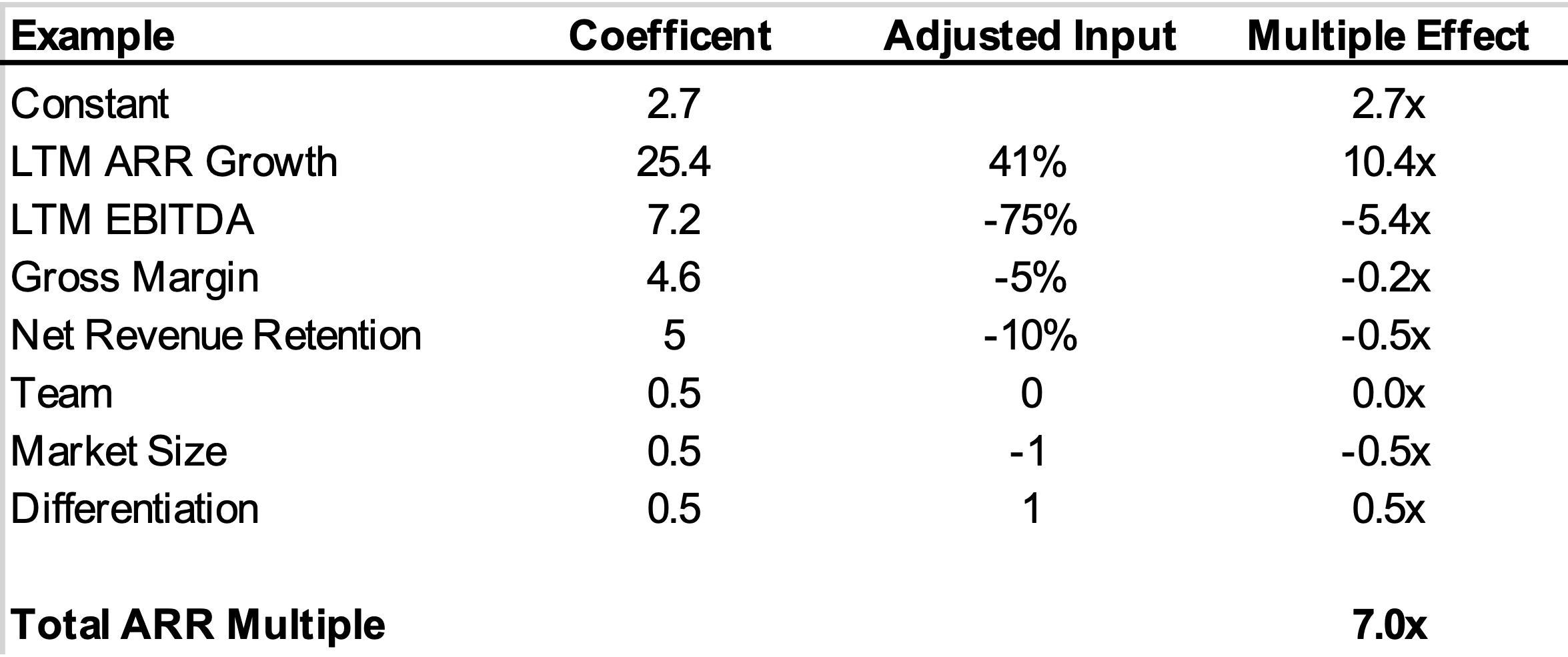

Brand-new SaaS valuation method just dropped (patent pending). I call it the Scorecard Method as it adjusts a company's valuation based on seven different inputs.

With my first attempt, I adjusted the multiples anecdotally based on my own hunch. After some self-reflection, I realised this wasn’t going to stand up to much rigour. I can’t really expect an auditor to okay a reference to “trust Cillian’s hunch”. So, I employed some statistics (another rare occasion where my Major in Mathematics came in useful).

I explored a list of 200 public software companies, played around with multivariate regression and found some statistically significant predictors of SaaS valuations being, NTM Revenue Growth %, NTM EBITDA Margin % and Gross Margin %. Unsurprisingly, Revenue growth is the most significant at nearly 3.5x more impactful on ARR multiples compared to EBITDA margins. A good reason to stop using Rule of 40 which gives equal weighting to both.

Given the lack of data and overconfidence in my hunch I added four more variables which impact your company’s ARR multiple - Net Revenue Retention, Team, Market Size and Differentiation.

To start on the model, we need to make some adjustments to the seven inputs so they fit the equation (detailed explanation in the video). Note Team, Market Size and Differentiation are qualitative inputs ranked 1 - 5 (five being the best).

To build the equation, I took the coefficients of NTM Revenue Growth %, NTM EBITDA Margin % and Gross Margin % from the regression and came up with my own coefficients for Net Revenue Retention, Team, Market Size and Differentiation. The equation is below.

ARR Multiple = 2.7 + 25.4xA*+ 7.2xE* + 4.6xG* + 5xN*+ 0.5xT* +0.5xM* + 0.5xD*

An example below shows how the equation works. You multiply your adjusted input by the respective coefficient. The products are added up to generate a company’s ARR Multiple.

Given public company growth levels are much more constrained than private companies, I’d imagine this model overemphasises growth. In any case, it’s a new and more detailed way to value your SaaS business. If you want the Excel, please let me know.

Generative AI Disrupting Pricing

The hype on Generative AI continues. Which type of startups or enterprises will win/benefit is a hot topic and one for a later date. One thing that seems like a good possibility is a reduction in the number of people needed to do certain tasks. Think customer service. If generative AI can handle 20% of interactions, you will theoretically need fewer agents. This is bad news for B2B SaaS companies selling to customer service agents who price on a per-user basis. Soon, it may no longer make sense to price based on users. Particularly if your value proposition is reducing the number of people you price against.

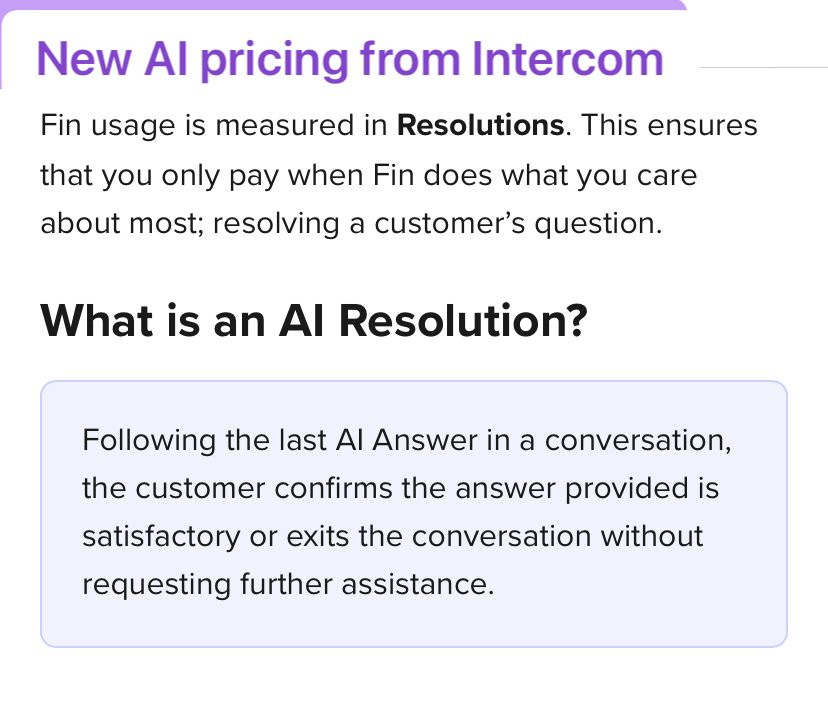

This threat to existing pricing structures is already causing some big moves in the tech world, most notably Intercom. Intercom, which charges per user for access to its platform, recently announced a new chatbot. This chatbot will cannibalise its own revenue. However, the new feature is moving away from user-based pricing. They now charge for each successful customer resolution by their AI chatbot. This is quite smart as the better the chatbot performs, the more money they will generate which should compensate for the reduction in users.

While user-based pricing has its benefits in simplicity, it has serious drawbacks as future growth is capped to users (not so good in a rapidly automating world), plus users share licenses unknowingly to the vendor. If you price based on users, now is probably a good time to start thinking about new pricing models. The optimal pricing strategy is very much bespoke to each company but should ideally score high on all of the following:

Linked to the customer value

Scalable - Grows with the customer usage

Auditable - Not gameable by the end customer

Predictable - Customers have visibility for the next 12 months at least (otherwise CFOs will not sign the contract)

Acceptable to customers

Metaverse Revival?

The metaverse hype seems a long way off the fever pitch days when Facebook rebranded to Meta and digital apes were the latest great investment. The Hype has definitely waned, but Apple has put a significant stamp of approval on the space with its latest product announcement. You can see the detailed review in the video as I’m not a big enough tech nerd to give a good view.

The thesis I love about the metaverse, assuming you nail virtual reality (photorealism, haptics, motion etc.), is that it solves so many massive problems, at least in a virtual sense. For one it breaks the laws of physics and enables teleportation. You can travel from London to anywhere instantly. It solves the need for nice housing as you can live on a thousand-acre farm in a mansion at a minimal cost. No more cosmetic surgery is required as you can pick an avatar, no more traffic accidents, no more plane crashes, there are endless problems solved if the metaverse can equate to real life.

Ignoring the moonshot applications that are probably decades away, Apple’s new Vision Pro really impressed me. The headset seems to display your own environment in near photorealism. This is a big step change from any of the cartoon VR environments I have been in. With Apple’s device today, it seems like you could remove the need for a home office or even a TV/cinema set-up (assuming you live alone) which is a good start when it comes to real-world value.

The obvious downside is the price but I’m sure there are plenty of tech enthusiasts who will buy one. The hope is that there are enough of these tech enthusiasts to make Apple invest in new product versions. Generally, the release should be good for the space and may drive some renewed interest in cheaper headsets, namely Oculus. I think it provides some upside for Zuckerberg over the next five to ten years.

Productivity Tech

Superhuman is a next-generation email software provider. It’s an attack on the very well-entrenched Outlook and Gmail positions. They differentiate on much better UX, speed and shortcuts. I have been using it for the past three months and will be sticking with it. The main benefits for me are (1) Template replies that can populate first names etc, (2) Deliverability stats and (3) shortcuts. The calendar features aren’t as good as Outlook but otherwise, it is streets ahead. Highly recommend.

Kennet Partners’ Investment Target

Kennet Partners is a Growth Equity investor with over 20 years of experience partnering with European and US SaaS companies. If you know any companies which fit our criteria, please reach out.

Investment size: $8m - $30m

Maturity: Over $3m in ARR

Growth: > 30%

Type: Bootstrapped and capital-efficient B2B SaaS businesses

Geography: Europe & US

Disclaimer: None of the content in the Newsletter should be taken as financial advice.